Updated June 11, 2021

We receive a lot of questions from contractors about our process and product. This blog post has the answers to some of our most commonly asked questions.

Have a question that isn’t answered here? Check out our Help Center for more FAQs!

Why should I offer financing?

If you don’t offer financing, you’re limiting the number of deals you can close. 69% of Americans have less than $1,000 saved. They might need your services — but don’t have the cash on hand to pay for it. By offering them financing, you’re enabling them to receive the funding they need to start a project now and pay back the funds over time.

Financing can allow homeowners to:

Address an emergency project (like a leaky roof) when they don’t have enough cash on hand to pay for it out of pocket.

Enjoy the ease of monthly payments rather than taking a lump sum out of their bank account at once.

Have the flexibility to upgrade their project

By offering financing options, you can appeal to these homeowners, expand your customer base, and grow your business — and your bottom line!

Is Hearth a bank?

No, Hearth is a software that helps contractors offer personal loans to their clients quickly and easily.

Banks and other financing institutions can take weeks to process and approve a loan application. Homeowners may spend valuable time and energy applying for a bank loan, wait weeks for an answer, and then scramble to find another source of funding if their application is rejected.

With Hearth, homeowners can see their loan options within 60-90 seconds without any effect on their credit score, can apply for the loan right on the lending partner’s website, and receive the funds within 1-3 days.

What is a personal loan?

Personal loans are the financing option that homeowners find through Hearth. With personal loans, homeowners receive the funding upfront and pay it back in monthly payments over a set period of time.

This type of loan doesn’t require any home equity and can be used for any sort of project, whether it’s HVAC, roofing, landscaping, or something else entirely.

What is Profit Protection Financing?

Profit Protection Financing is a type of financing focused on protecting your profits. Because Hearth offers Profit Protection Financing, we don’t charge any per-loan dealer fees. Instead, every cent you make stays with you.

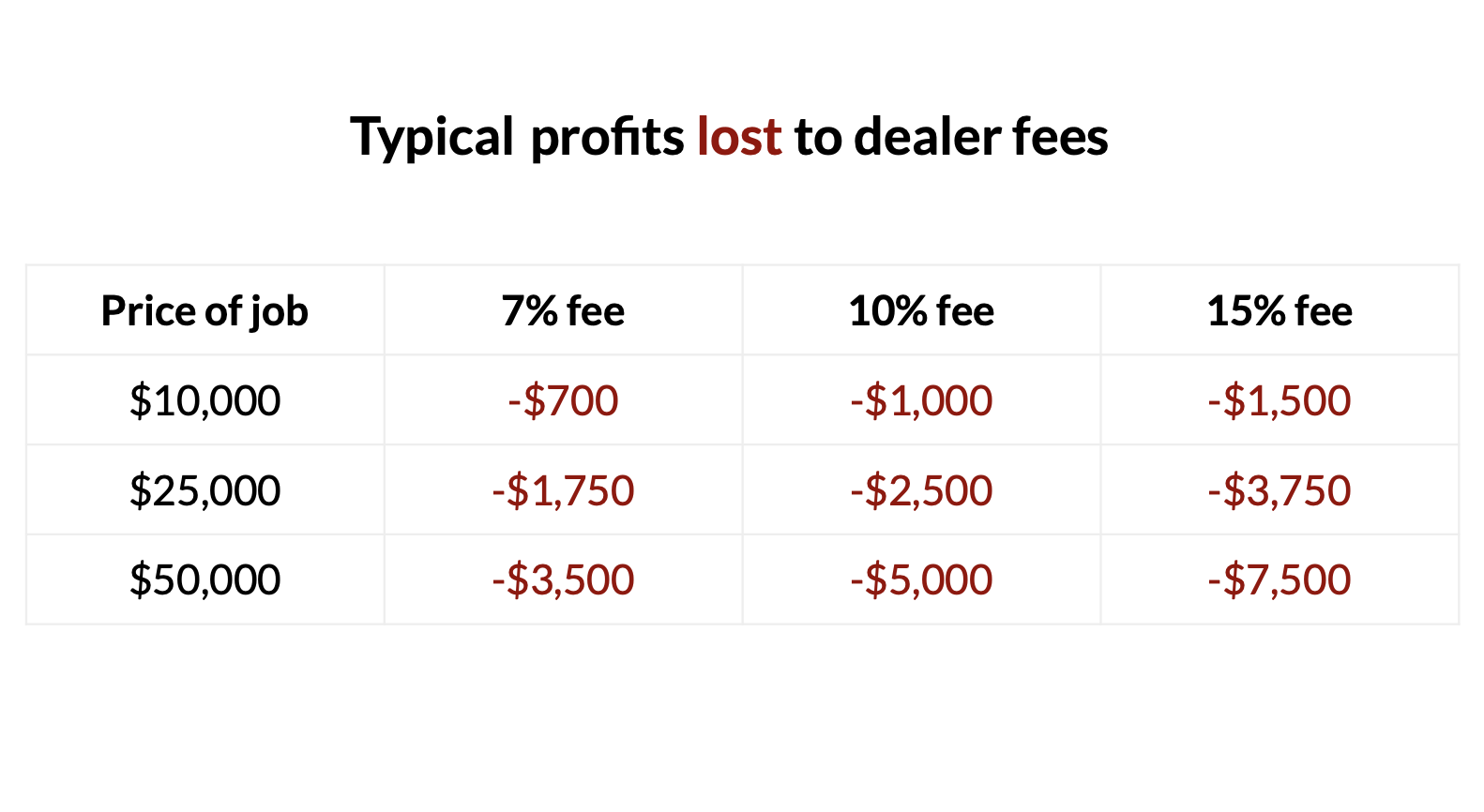

Other financing companies offer Buy-Down Financing where you, as a contractor, buy down your client’s rates to show them lower rates than they would’ve seen otherwise. You’ll typically be charged about 7-15% of every job: a cost known as a dealer (or merchant) fee. That amount comes out of your profit margin and goes to a third-party financing provider.

The following chart shows you how much you could lose in dealer fees for a single job!

For more information on the different types of financing, check out The Contractor’s Handbook: How to pick the right financing option to grow your business.

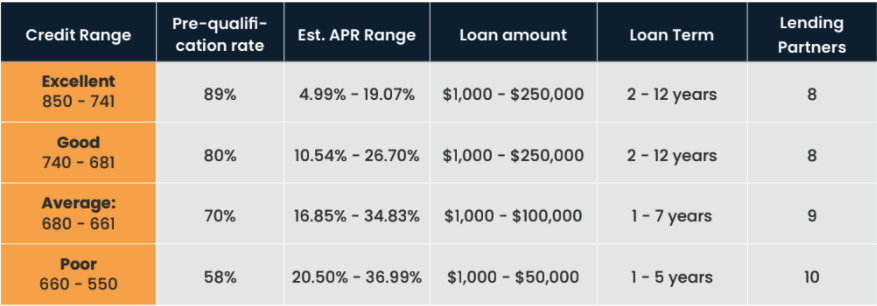

What rates can my homeowner expect with Profit Protection Financing?

If you offer Profit Protection Financing through Hearth, your clients can expect to see the following rates. The majority of clients will see options with APRs in the ranges listed below, but some may receive options with lower or higher APRs. Exact rates depend on your client’s financial profile and the lending partner’s unique model.

Why do the funds go to the homeowner and not to the contractor?

Hearth doesn’t want you to be liable for the loan. If the loan isn’t paid in time or in full, the lending partner will work directly with the homeowner so you don’t have to worry about fielding calls, following up with clients, or managing paperwork.

How do I get paid?

Working with a homeowner who receives funding through one of Hearth’s lending partners is the same as working with a cash-in-hand homeowner. The homeowner receives the full loan amount upfront, and you can work with them to set a payment schedule and confirm it through your usual process and/or with your usual contract.

Hearth Contracts is included in your membership and gives you access to custom contract templates and the ability to secure digital signatures from your customers. Learn more here.

The homeowner pays back the loan to the lending partner in fixed monthly payments.

Included in your Hearth membership is Hearth Pay, an easy way to collect digital payments from your customers. Send payment requests, collect payments, and send your funds to your bank account all from your mobile device. To learn more click here.

Why does Hearth have a subscription fee?

Hearth’s annual subscription allows you access to unlimited loans with no dealer fees and access tools to help your business grow.

With Hearth you’ll:

Save thousands of dollars in dealer fees

Access sales tools to make talking money and closing deals easier

Technology to track loan statuses, create digital contracts, and collect payments all from your smartphone

Do you have a rewards program?

Yes, our Referrals Rewards Program means that you can earn at least $250 for every contractor you refer and sign up with Hearth. Visit this link to join.

Once you fill out the form, you’ll receive an email from a member of our team with steps on how to refer and when to expect your rewards.

If you’re not a contractor yourself but you work with contractors who want to offer financing, you may be a good fit for our affiliate program! Click this link to learn more.

What support will I receive?

We have a dedicated customer success team who can answer any questions you or your customers have. The response time will vary based on your subscription plan but will be no more than 48 hours.

Have a question we didn’t answer here? Visit our Help Center for more questions and answers.

——

*For each self-reported credit score range, pre-qualification rate is calculated by dividing the number of pre-qualified Hearth users by the total number of users who submitted a loan request.

**For pre-qualified Hearth users with this credit score range, our lending partners returned loan options with this range of minimum APRs for the 65% of pre-qualified users with minimum APRs between the 10th and 75th percentiles.

***For example, a loan in the amount of $10,000 for a term of 5 years with an APR of 6.00% would be repaid over 60 monthly payments in the amount of $193.33.