You may have heard that you’ll be seeing green only if your client has a premium FICO score. Is that true?

The short answer is no — not with Hearth.

We’ve broken down some other common questions and misconceptions about FICO scores below:

Question: What is a FICO score?

Answer: A FICO score is a credit score that ranges from about 300 (a poor/low credit score) to 850 (an excellent/high credit score). The score is calculated from credit report data, including payment history, amount(s) owed, length of credit history, new credit, and types of credit in use.

Lending partners look at homeowners’ FICO scores–along with requested loan amount, credit history, and income–both when they’re deciding whether to offer a loan and when they’re calculating the loan terms (such as the payback period and the interest rates).

Question: Does a low FICO score mean that the homeowner doesn’t manage their money well?

Answer: No. FICO scores can be affected by life events (including marital status and child expenses) — some of which may be beyond your homeowners’ control.

Question: My clients have low FICO scores. Does that mean they automatically won’t qualify for a loan?

Answer: With Hearth, clients with low FICO scores should not be afraid to request financing.

According to FICO, more than 79 million Americans (24% of the U.S population) have FICO scores below 680. But, despite this number, many lending partners — including institutions such as banks or credit unions — don’t even have options for these “less than premium” scores. They believe that these homeowners are too risky — too likely not to pay back the loan in time or in full — of an investment.

Hearth, on the other hand, works with a network of lending partners, and they all work with a range of FICO scores and evaluate them differently when deciding the terms of a loan. As a result, a high FICO is not an automatic guarantee that your client will get a loan offer or favorable loan terms through Hearth and a low FICO score is not an automatic guarantee that your client won’t get a loan offer or favorable loan terms through Hearth.

We find competitive payment options for around 70% of homeowners who request options through Hearth. We’re also constantly adding new lending partners to our network to expand the competitive payment options we can offer your clients, regardless of their FICO score.

Question: What can my client expect if they try to prequalify through Hearth?

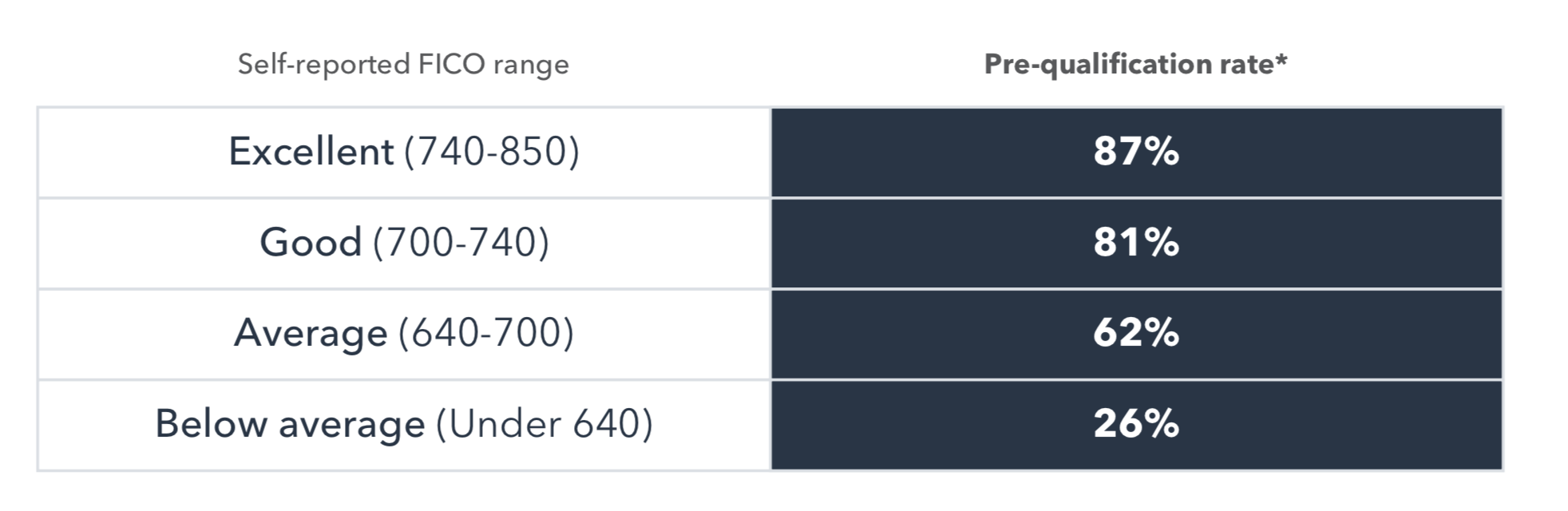

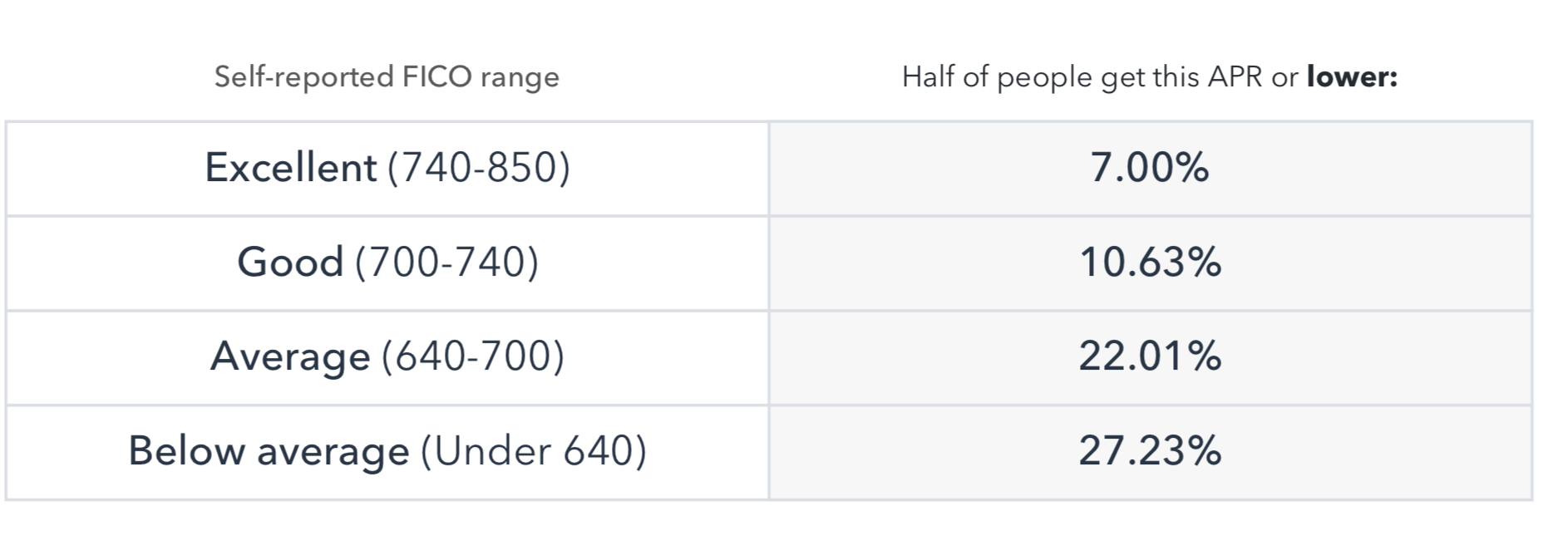

Answer: FICO scores is one factor that affects the rates that your client sees. Rates will increase and the odds of pre-qualification will decrease as your client’s FICO score decreases.

Question: Does prequalifying through Hearth affect my client’s credit score?

Answer: No, it doesn’t. Be sure to remind your clients that Hearth allows them to check their rates without affecting their credit scores.

Question: Should my clients feel limited by their FICO scores?

Answer: Absolutely not! Don’t let a less-than-perfect score drag your clients–or you!–down. A FICO score is not the be-all-end-all when it comes to prequalifying, securing a loan, and starting a project.